The Board Is Closed

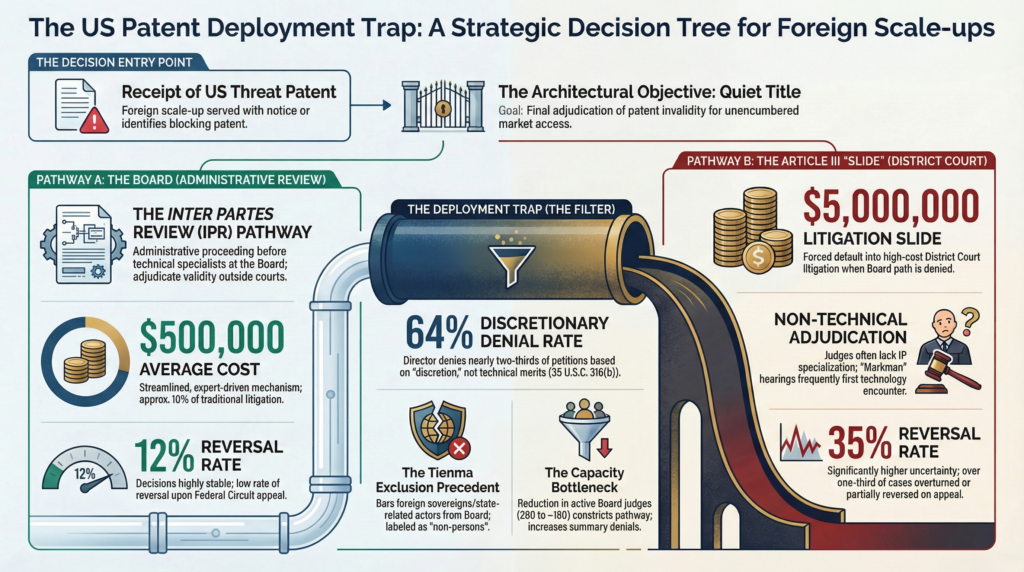

A 64% discretionary denial rate. An institution rate of approximately 20%. The Inter Partes Review mechanism — the AIA’s central promise of a cheaper, faster path to patent invalidity — has been functionally decommissioned. The question is not whether this happened. It is whether your deployment architecture accounts for the closure of the Board.

The America Invents Act of 2011 made a specific promise to the technology industry. If a bad patent was blocking your product, you had an alternative to the $5 million district court gauntlet. You could challenge it before the Patent Trial and Appeal Board for approximately $500,000 — a tenth of the cost, a fraction of the timeline, and without the discovery exposure that makes district court litigation existentially dangerous for companies whose core architecture has never been scrutinised under oath.

That promise has been systematically withdrawn. Not through legislation. Not through a court ruling. Through a series of administrative manoeuvres executed under 35 U.S.C. §316(b) — a provision granting the Office Director discretionary authority over institution decisions — that has concentrated power over the Board’s docket into a single office with no written explanation requirement and no meaningful appellate check.

The result is an institution rate that has collapsed to approximately 20 percent, driven by a discretionary denial rate of 64 percent. The Board still exists. It simply no longer functions as a predictable defensive instrument for the entities that need it most.

The Discretionary Chokehold

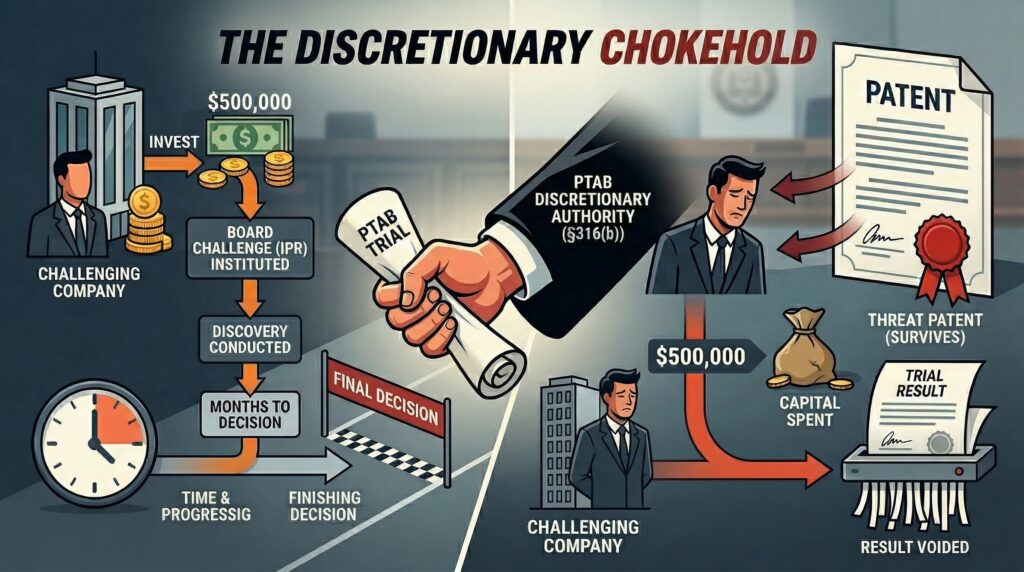

Think of the Board’s institution process as a load balancer sitting in front of your litigation infrastructure. Under the AIA’s original architecture, a petition meeting the statutory threshold — demonstrating a reasonable likelihood that at least one claim was unpatentable — would be instituted for trial. The load balancer had clear routing rules. If your packet met the criteria, it went through.

The Director’s aggressive application of §316(b) has replaced those routing rules with a single-point authority that can drop packets for any reason, with no obligation to explain why. Discretionary denials now account for the majority of rejections before the Board even reaches the merits of a challenge. A petition can be technically impeccable — prior art clearly on point, claim mapping airtight — and still be denied on discretionary grounds that the Office is not required to articulate in writing.

The instability goes further. The Director has established a precedent of retroactively withdrawing institution decisions on trials that are nearing their one-year statutory deadline for final written decisions. A company that has invested $500,000 in a Board challenge, survived institution, conducted discovery, and is months from a decision can find that trial pulled back under §316(b) before the final decision issues. The capital is spent. The result is voided. The threat patent survives.

For a funded scale-up, this is expensive and disorienting. For a pre-Series A company that scraped together $500,000 specifically because it could not afford the $5 million alternative, it is terminal.

The Foreign Exclusion Architecture

The discretionary chokehold is general — it applies to any petitioner. The RPI disclosure regime is specific. It was engineered with a particular category of challenger in mind.

The reinstatement of the Corning Optical precedent mandates exhaustive Real Party in Interest disclosures. Every entity with a financial stake in the outcome of a Board challenge must be identified. Including every investor. And every co-challenger. Every entity in the funding chain that could benefit from invalidation of the target patent.

For a domestic challenger, this is an administrative burden. For a foreign-backed entity — a scale-up whose Series A includes sovereign wealth fund participation, a strategic investor from a jurisdiction the Office has flagged as a threat actor, or a company whose cap table includes any state-adjacent institution — it is a structural trap.

The Tienma decision completed the architecture. The Board held that foreign sovereigns and state-backed actors do not qualify as “persons” under the AIA. The statutory text defines who can petition for inter partes review. Foreign sovereigns are not within that definition. The precise legal reasoning is cynically elegant: the Office itself is not a “person” under certain statutory frameworks, and it applied the same definitional exclusion to lock out foreign state actors — using a carveout designed to limit the government’s own legal exposure as a weapon against non-domestic challengers.

Pair these two decisions and the system topology becomes clear. The RPI disclosure requirement forces foreign-backed entities to reveal their full investor architecture. The Tienma exclusion then uses that revealed architecture to determine whether the petitioner qualifies as a person entitled to petition at all. The disclosure is not just an administrative requirement. It is the identification protocol that feeds the exclusion mechanism.

The Counter and Its Failure

The administration’s stated rationale for this regime is defensible in isolation. The VLSI patent challenge — in which entities called Open Sky and PQA filed serial IPR petitions against VLSI’s patents after Intel had already been hit with a $2.18 billion jury verdict — demonstrated genuine abuse of the Board’s mechanism. Anonymous, opaque entities were weaponising serial filings to harass patent holders and destabilise licensing negotiations that domestic manufacturers had already concluded.

The “one join and done” doctrine addresses this specifically. Under the new Notice of Proposed Rulemaking, serial IPR filings on the same patent are prohibited. A challenger gets one coordinated petition. If it fails, the patent is effectively shielded from further Board challenge regardless of whether new prior art surfaces later.

The abuse this prevents is real. The collateral damage it creates is structural and indiscriminate.

Removing the serial filing mechanism does not just neutralise bad actors. It eliminates the sequencing strategy that legitimate challengers use to manage invalidity campaigns against complex, multi-claim portfolios. A hostile incumbent with a portfolio of forty interconnected patents protecting a single technology vertical does not present forty independent challenges. It presents a coordinated topology of overlapping claims designed to survive any single attack vector. A challenger that can only join one IPR petition per patent and cannot sequence challenges as prior art is discovered has lost the ability to map and dismantle that topology systematically.

The doctrine that was designed to stop anonymous entities from gang-tackling individual patents has simultaneously prevented legitimate entities from executing the only strategy that works against a distributed portfolio attack.

What Removing the Board (Pressure Valve) Actually Does

A system under pressure needs a relief mechanism. When you remove the relief mechanism, pressure does not dissipate — it redirects.

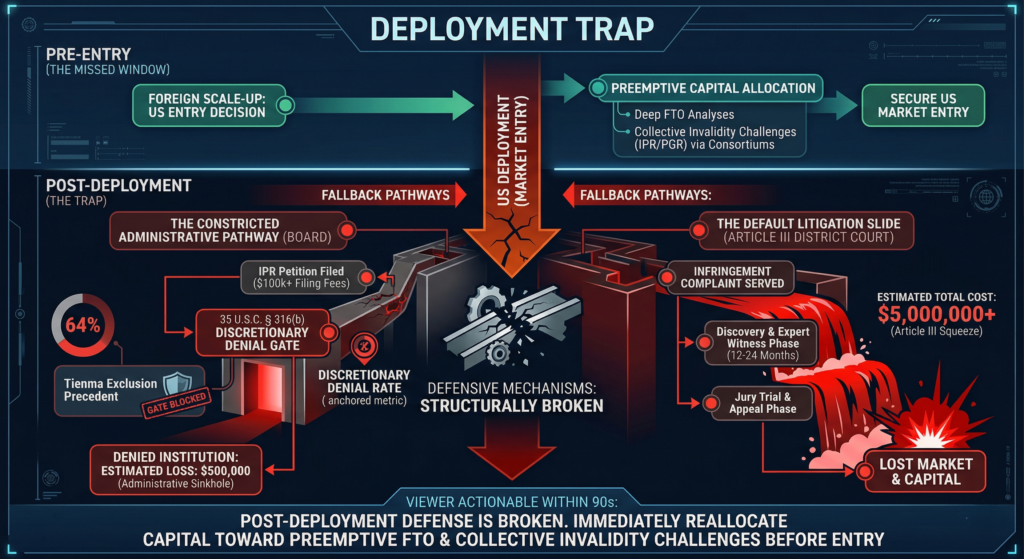

The Board was the patent system’s pressure valve. Disputes that were too expensive for district court but too threatening to ignore could be routed through the Board at a cost that did not immediately bankrupt the challenged party. The $500,000 figure is not trivial. But it is survivable for a company that has reached Series A. It is a fraction of what it costs to defend a district court infringement action through trial.

With the Board’s institution rate at 20 percent and the discretionary denial rate at 64 percent, the pressure valve is functionally closed. Disputes that would previously have been routed through the Board now have two destinations: settlement or district court.

Settlement at gunpoint is not a neutral outcome. A company that settles an infringement claim against a bad patent is paying a licensing royalty on technology it has a right to use. It is also signalling to every other holder of weak IP in its technology space that it is a viable extraction target. The settlement does not close the threat — it advertises a price.

District Court is Worse than the Board

The discovery process in patent litigation is not a search for truth. It is a compelled disclosure mechanism that forces both parties to produce internal documents, technical specifications, deployment architectures, and communications that either party would never voluntarily reveal. For a foreign scale-up whose core competitive advantage is its deployment topology — the specific technical choices that differentiate its product — district court discovery is not just expensive. It is a forced disclosure of the architecture to the very incumbent that is trying to block it.

The average cost of patent litigation through trial is $5 million per side. That figure assumes a functioning dispute that proceeds through the standard timeline. It does not account for the asymmetric resource differential between a well-capitalised incumbent and a Series B company. Nor does it account for the injunction risk that can halt product deployment while litigation proceeds. It also does not account for the reputational signal that an infringement lawsuit sends to prospective investors in the middle of a funding round.

For a pre-Series A entity, the arithmetic is straightforward. The Board off-ramp at $500,000 was already at the edge of survivable. The district court alternative at $5 million is not a harder path — it is not a path at all. The outcome of closing the Board to this category of challenger is not that disputes get resolved in district court. It is that disputes get resolved through immediate settlement on the patent holder’s terms, because no alternative exists.

The Preemptive Architecture

The defensive posture that assumed the Board would be available as a post-lawsuit off-ramp is no longer viable. The institution rate is 20 percent. The discretionary denial rate is 64 percent. The serial filing mechanism is being eliminated. The RPI disclosure regime is designed to identify and penalise foreign-backed challengers. The Tienma exclusion bars state-adjacent actors from petitioning at all.

The architecture that works in this environment is not reactive. It is preemptive.

Freedom-to-operate analysis cannot be a pre-launch checklist item. It has to be a continuous intelligence function that maps the patent landscape of your technology vertical before you begin US market deployment — not after you receive a demand letter. Blocking patents do not become blocking patents the day the demand letter arrives. They become blocking patents the day they issue. The window for cost-effective action is the period between issuance and the moment your product is in the US market at scale, because that is the moment when an infringement action becomes immediately actionable and the leverage dynamic shifts entirely to the patent holder.

Coordinated, preemptive invalidity challenges — executed before US market entry by a coalition of entities with aligned interests against the same blocking portfolio — are the available alternative. The “one join and done” doctrine restricts serial individual challenges. It does not restrict a well-structured collective petition filed before any infringement dispute exists. The petitioner coalition assembles prior art collectively, coordinates claim mapping across the portfolio, and executes a single coordinated challenge at the moment of maximum leverage — when the patent holder has no active district court action to use as a blocking mechanism and no injunction to threaten.

Capital for Lack of the Board

This requires capital allocation that most deployment architectures do not currently include. Freedom-to-operate analysis at the required depth is not a $50,000 engagement. Coordinated invalidity campaigns require legal infrastructure, prior art search capacity, and coalition management that functions more like a shared defensive facility than a standard legal budget line.

The companies that understand this environment are building that infrastructure now, before they need it. The companies that do not understand it are carrying a $5 million contingent liability on every product they are planning to bring into the US market.

Reallocate the capital before the demand letter arrives. The Board will not be there when it does.

— Stars and Sand US Patent Strategies for the World